Tax Traps in a Debt Crisis: What I Learned the Hard Way

Facing a debt crisis, I thought smart tax planning would be my escape route—until I fell into costly mistakes. What I didn’t know about deductions, timing, and legal boundaries ended up deepening my financial hole. This is my real story of missteps, lessons, and the hard-earned wisdom that finally brought clarity. If you're struggling with debt, this could save you from the same pitfalls. I learned that when financial pressure mounts, the line between clever strategy and dangerous misstep becomes dangerously thin. What seemed like a shortcut to relief only led to more stress, penalties, and regret. But from that pain came insight—insight that reshaped how I manage money, taxes, and responsibility.

The Breaking Point: When Debt Overwhelmed My Finances

There was a moment, unmistakable and sobering, when I realized I was no longer managing my finances—I was surviving them. Credit card balances had crept upward for years, masked by minimum payments and temporary balance transfers. Then came an unexpected job reduction, a medical bill for a family member, and suddenly the fragile equilibrium collapsed. Monthly income barely covered essentials, let alone the growing pile of debt. Late fees accumulated, interest rates climbed, and the emotional toll was just as heavy as the financial one. Sleepless nights became routine, and every envelope with a bank logo felt like a personal indictment.

It was in that state of urgency that I turned to taxes as a potential lifeline. I had heard stories of people using tax refunds to pay off credit cards, or reducing their tax liability to free up cash. To me, the tax system seemed like a puzzle with a solution—if only I could find the right combination of deductions and credits, I might unlock enough money to catch my breath. I convinced myself that aggressive tax planning wasn’t manipulation; it was resourcefulness. I didn’t yet understand that tax strategy, when divorced from overall financial health, can become a trap rather than a tool.

What I failed to see was that my approach was reactive, not strategic. I wasn’t building a sustainable financial future—I was trying to borrow from next year’s income to fix this year’s crisis. The pressure to act quickly clouded my judgment. I overlooked the importance of accuracy, documentation, and long-term consequences. My goal was immediate relief, not lasting stability. And in that desperation, I set myself up for a series of decisions that would make my debt crisis worse, not better.

The Allure of Quick Fixes: Misguided Tax Strategies That Backfired

When you’re drowning in debt, every dollar counts—and I became obsessed with finding ways to keep more of my income, even if it meant stretching the rules. One of my first missteps was claiming a home office deduction far beyond what was justifiable. I worked from home occasionally, but not as a formal remote employee or self-employed professional with a dedicated workspace. Still, I calculated square footage, deducted a portion of rent, utilities, and even internet, convinced I was entitled to relief. I told myself it was common practice, that many people did it. What I didn’t do was keep detailed logs, time records, or receipts to substantiate the claim. To the IRS, intent doesn’t override documentation.

Later, when I filed, I also deferred income by delaying freelance payments into the next tax year, believing I could lower my current taxable income and reduce my tax bill. What I didn’t anticipate was that this would disrupt my cash flow when I actually needed the money most. By pushing income forward, I created a gap in available funds during a critical repayment window. Meanwhile, the tax savings were minimal—less than $400—and not nearly enough to make a dent in my debt. The real cost came later, in the form of scrutiny and corrections.

Another mistake was overclaiming business expenses. I had started a small side project selling handmade goods online, and I began categorizing personal purchases—like a new laptop, printer, and even a portion of my phone bill—as business costs. While some of these could have qualified under the right circumstances, I lacked clear separation between personal and business use. I didn’t maintain a separate bank account or track usage percentages. In my mind, I was investing in a future income stream; in reality, I was blurring financial lines in a way that invited risk.

These strategies weren’t inherently illegal, but they were dangerously misapplied. Tax tools like deductions and deferrals are designed for structured, documented financial behavior—not for crisis-driven improvisation. I treated tax planning like a game of optimization without understanding the rules of engagement. The result? A return that looked good on paper but couldn’t withstand review. When the IRS sent a notice questioning my claims, the stress returned, sharper and more specific. I had tried to use taxes as a shortcut, but I ended up paying a higher price.

Why Timing Matters: How Poor Planning Made My Debt Worse

One of the most underestimated aspects of financial management is timing—especially when taxes and debt intersect. I learned this the hard way when I delayed filing my return to hold onto cash for debt payments. I told myself I was being practical: better to pay the credit card than send money to the government. But by missing the April deadline, I triggered late-filing penalties and interest on any tax due. What I thought was a temporary reprieve became a compounding obligation.

Even worse, I underestimated my tax liability and failed to make quarterly estimated payments. As someone with irregular income, I was responsible for paying taxes throughout the year, but I skipped payments to prioritize credit card minimums. The logic seemed sound at the time: avoid high-interest debt first. But the IRS doesn’t negotiate. When tax season arrived, I owed not only the original amount but also penalties for underpayment. The total was over $900—money I didn’t have and couldn’t borrow without worsening my debt cycle.

Another timing error was holding onto my tax refund. I had always treated the refund as a bonus, a windfall to spend or allocate freely. But during my crisis, I delayed filing specifically to keep that refund as a future safety net. I thought: “If I file now, I’ll be tempted to use it. If I wait, I can time it with a big payment.” But delaying meant I lost the opportunity to use that money strategically earlier in the year. By the time I received the refund, my debt situation had deteriorated further, and the amount—while helpful—was no longer enough to make a meaningful difference.

These timing missteps created a domino effect. Each decision, made in isolation, seemed reasonable. But together, they amplified my financial strain. I was trying to manage two systems—tax and debt—without seeing how they influenced each other. I treated tax obligations as secondary to debt repayment, not realizing that neglecting one could destabilize the other. The lesson was clear: financial health requires coordination, not compartmentalization. When timing is off, even well-intentioned moves can backfire.

The Hidden Costs of DIY Tax Moves During Financial Stress

In my effort to save money, I made what I thought was a sensible choice: I prepared my own taxes using affordable software. I had done it before without issue, and the cost of a professional—often $200 to $500 or more—felt like an unaffordable luxury. I told myself I could handle it, that the software would guide me correctly. What I didn’t account for was the hidden cost of error—the financial and emotional toll of getting it wrong when I could least afford it.

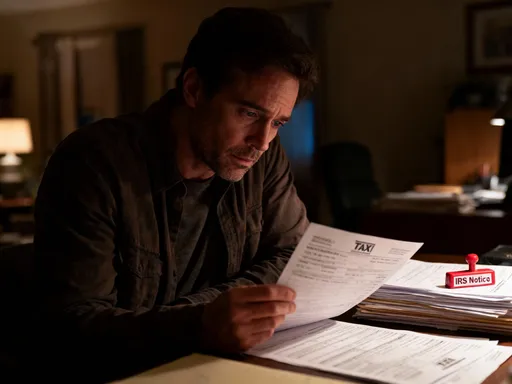

The first sign of trouble came in the form of a letter from the IRS. It wasn’t a notice of audit, but a CP2000 form—a proposed adjustment to my return. The agency had matched third-party records (like 1099s from banks and clients) to my filing and found discrepancies. My claimed deductions didn’t align with reported income, and some expenses lacked substantiation. The letter requested documentation and threatened additional taxes, penalties, and interest if unresolved.

The anxiety that followed was intense. Every mail delivery brought dread. I spent hours gathering receipts, writing explanations, and responding to IRS correspondence. The process took weeks, and by the time it was resolved, I owed an additional $680. I had saved $400 by not hiring a professional, but I ended up paying nearly double that in corrections and penalties. The false economy was clear: short-term savings led to long-term costs.

Beyond the money, the experience damaged my confidence. I began to question every financial decision I made. What else had I gotten wrong? Were there other liabilities lurking? The stress of uncertainty became its own burden. A qualified tax professional could have caught the red flags before filing—flagged the aggressive deductions, advised on proper documentation, and ensured compliance. They could have helped me understand how to legally reduce liability without crossing into risky territory. Instead, I went it alone and paid the price.

This wasn’t just about technical errors. It was about perspective. When you’re in a debt crisis, your thinking narrows. You focus on immediate relief, not long-term consequences. A professional brings objectivity, experience, and structure—qualities that are hard to access when you’re overwhelmed. I learned that financial stress is not the time to cut corners on expertise. The cost of guidance is far less than the cost of correction.

Separating Smart Planning from Dangerous Shortcuts

The turning point in my journey came when I stopped seeing taxes as a source of quick cash and started viewing them as part of a broader financial system. I began to understand the difference between tax optimization—legal, sustainable strategies that improve cash flow—and tax avoidance that borders on recklessness. The line isn’t always bright, but it exists, and crossing it can have serious consequences.

True tax planning isn’t about squeezing every possible dollar from the system. It’s about aligning your tax strategy with your actual financial behavior. For example, adjusting your W-4 withholding to receive a smaller refund throughout the year—rather than a lump sum—can give you more control over cash flow. That extra money in each paycheck can go directly toward debt repayment, reducing interest and shortening payoff timelines. It’s not a dramatic move, but it’s consistent and sustainable.

Another smart practice is using tax-advantaged accounts wisely. I began contributing to a traditional IRA, not to avoid taxes entirely, but to reduce taxable income in a year when I still had some discretionary income. The deduction was modest, but it was legitimate and well-documented. More importantly, it reinforced disciplined saving. I wasn’t gaming the system—I was working within it.

I also learned to time deductions strategically. Instead of claiming expenses I wasn’t entitled to, I planned for those I could legitimately use. For example, I bundled medical expenses in a single year to exceed the threshold for itemized deductions. I scheduled necessary home repairs to qualify for energy efficiency credits. These moves required planning and patience, but they were legal, ethical, and effective.

The key shift was mindset. I stopped asking, “How can I reduce my tax bill this year?” and started asking, “How can I manage my taxes in a way that supports my long-term financial health?” That simple reframe changed everything. It moved me from desperation to discipline, from shortcuts to sustainability.

Building a Realistic Tax Strategy That Supports Debt Recovery

Recovery didn’t happen overnight. It came from consistent, small decisions that added up over time. I developed a tax strategy that was no longer separate from my debt plan—but integrated with it. The first step was creating a quarterly financial review. Every three months, I assessed my income, expenses, tax obligations, and debt payments. I set aside a portion of income specifically for taxes, treating it like any other bill. This eliminated the surprise of a large tax bill and reduced the temptation to underpay.

I also began filing early, even if I couldn’t pay the full amount. I learned that filing on time avoids late-filing penalties, even if you request a payment plan. The IRS offers installment agreements that, while not ideal, are far less costly than penalties and interest from non-filing. I applied for one and committed to consistent payments. It wasn’t glamorous, but it restored compliance and control.

When I received a tax refund, I stopped treating it as discretionary income. Instead, I directed it entirely toward my highest-interest debt. One year, the refund was $1,200. I used every dollar to pay down a credit card with a 24% interest rate. That single payment reduced my balance significantly and saved me hundreds in future interest. Over time, as my debt decreased, I redirected future refunds toward building an emergency fund—creating a buffer against future crises.

I also improved my recordkeeping. I created digital folders for receipts, bank statements, and tax documents. I tracked mileage for any legitimate business use, maintained time logs for home office claims, and separated personal and business accounts. These habits took effort, but they gave me confidence when filing. I no longer feared IRS notices because I knew my records were sound.

Most importantly, I accepted that progress isn’t linear. There were months when I fell short, when unexpected expenses derailed the plan. But I didn’t abandon the system. I adjusted, recalibrated, and kept going. The goal wasn’t perfection—it was persistence.

Lessons That Last: How I Turned Financial Failure into Lasting Wisdom

Looking back, I don’t regret the mistakes—but I do regret the assumptions behind them. I assumed that tax planning could rescue me from debt. I assumed that DIY was always cheaper. I assumed that urgency justified bending rules. Each of those beliefs was flawed, and each led me deeper into trouble. But from that experience, I gained something more valuable than a quick fix: wisdom.

I learned that financial health isn’t built on hacks or loopholes. It’s built on honesty—with yourself and the system. It requires humility to admit when you need help, discipline to follow through on commitments, and patience to let results unfold over time. I learned to see taxes not as an enemy to be outsmarted, but as a responsibility to be managed with care.

I also learned the value of professional guidance. I now consult a tax advisor every year, not because I can’t file alone, but because I value the oversight, the peace of mind, and the long-term perspective they provide. It’s a small investment that protects a much larger financial foundation.

Most of all, I learned that debt and taxes are not separate challenges. They are interconnected parts of a single financial reality. You cannot manage one effectively without considering the other. True financial stability comes from integration, not isolation. It comes from making decisions not for immediate relief, but for lasting resilience.

If you’re facing a debt crisis, know this: there are no magic solutions. But there is a path forward—one built on clarity, consistency, and courage. Avoid the traps I fell into. Seek help when you need it. Respect the rules. And remember: the goal isn’t just to survive the crisis, but to emerge from it stronger, wiser, and more in control than before.